%20-%20http://www.bohemiancoding.com/sketch%20--%3e%3ctitle%3eIcon/Menu%3c/title%3e%3cdesc%3eCreated%20with%20Sketch.%3c/desc%3e%3cdefs%3e%3cpolygon%20id='path-1'%20points='0.0005%200.646%2022.386%200.646%2022.386%203.1455%200.0005%203.1455'%3e%3c/polygon%3e%3cpolygon%20id='path-3'%20points='0.0005%200.9341%2022.386%200.9341%2022.386%203.4341%200.0005%203.4341'%3e%3c/polygon%3e%3cpolygon%20id='path-5'%20points='0.0005%200.5%2022.386%200.5%2022.386%203%200.0005%203'%3e%3c/polygon%3e%3c/defs%3e%3cg%20id='Symbols'%20stroke='none'%20stroke-width='1'%20fill='none'%20fill-rule='evenodd'%3e%3cg%20id='Icon/Menu'%3e%3cg%20id='Group-10-Copy'%20transform='translate(3.800000,%205.300000)'%3e%3cg%20id='Group-3'%20transform='translate(0.000000,%200.354500)'%3e%3cmask%20id='mask-2'%20fill='white'%3e%3cuse%20xlink:href='%23path-1'%3e%3c/use%3e%3c/mask%3e%3cg%20id='Clip-2'%3e%3c/g%3e%3cpath%20d='M22.3865,2.6455%20C22.3865,2.9205%2022.1615,3.1455%2021.8865,3.1455%20L0.5005,3.1455%20C0.2245,3.1455%200.0005,2.9205%200.0005,2.6455%20L0.0005,1.1455%20C0.0005,0.8705%200.2245,0.6455%200.5005,0.6455%20L21.8865,0.6455%20C22.1615,0.6455%2022.3865,0.8705%2022.3865,1.1455%20L22.3865,2.6455%20Z'%20id='Fill-1'%20fill='%23FFFFFF'%20mask='url(%23mask-2)'%3e%3c/path%3e%3c/g%3e%3cg%20id='Group-6'%20transform='translate(0.000000,%207.354500)'%3e%3cmask%20id='mask-4'%20fill='white'%3e%3cuse%20xlink:href='%23path-3'%3e%3c/use%3e%3c/mask%3e%3cg%20id='Clip-5'%3e%3c/g%3e%3cpath%20d='M22.3865,2.9341%20C22.3865,3.2091%2022.1615,3.4341%2021.8865,3.4341%20L0.5005,3.4341%20C0.2245,3.4341%200.0005,3.2091%200.0005,2.9341%20L0.0005,1.4341%20C0.0005,1.1591%200.2245,0.9341%200.5005,0.9341%20L21.8865,0.9341%20C22.1615,0.9341%2022.3865,1.1591%2022.3865,1.4341%20L22.3865,2.9341%20Z'%20id='Fill-4'%20fill='%23FFFFFF'%20mask='url(%23mask-4)'%3e%3c/path%3e%3c/g%3e%3cg%20id='Group-9'%20transform='translate(0.000000,%2015.354500)'%3e%3cmask%20id='mask-6'%20fill='white'%3e%3cuse%20xlink:href='%23path-5'%3e%3c/use%3e%3c/mask%3e%3cg%20id='Clip-8'%3e%3c/g%3e%3cpath%20d='M22.3865,2.5%20C22.3865,2.775%2022.1615,3%2021.8865,3%20L0.5005,3%20C0.2245,3%200.0005,2.775%200.0005,2.5%20L0.0005,1%20C0.0005,0.725%200.2245,0.5%200.5005,0.5%20L21.8865,0.5%20C22.1615,0.5%2022.3865,0.725%2022.3865,1%20L22.3865,2.5%20Z'%20id='Fill-7'%20fill='%23FFFFFF'%20mask='url(%23mask-6)'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

'%20fill='%23fff'%20fill-rule='nonzero'%3e%3cg%20id='icon/fold'%20transform='translate(240.000000,%20272.000000)'%3e%3cpath%20d='M11.5,2.3%20C6.4216,2.3%202.3,6.4216%202.3,11.5%20C2.3,16.5784%206.4216,20.7%2011.5,20.7%20C16.5784,20.7%2020.7,16.5784%2020.7,11.5%20C20.7,6.4216%2016.5784,2.3%2011.5,2.3%20Z%20M10.58,18.7956%20C6.946,18.3448%204.14,15.2536%204.14,11.5%20C4.14,10.9296%204.2136,10.3868%204.3332,9.8532%20L8.74,14.26%20L8.74,15.18%20C8.74,16.192%209.568,17.02%2010.58,17.02%20L10.58,18.7956%20Z%20M16.928,16.4588%20C16.6888,15.7136%2016.008,15.18%2015.18,15.18%20L14.26,15.18%20L14.26,12.42%20C14.26,11.914%2013.846,11.5%2013.34,11.5%20L7.82,11.5%20L7.82,9.66%20L9.66,9.66%20C10.166,9.66%2010.58,9.246%2010.58,8.74%20L10.58,6.9%20L12.42,6.9%20C13.432,6.9%2014.26,6.072%2014.26,5.06%20L14.26,4.6828%20C16.9556,5.7776%2018.86,8.418%2018.86,11.5%20C18.86,13.4136%2018.124,15.1524%2016.928,16.4588%20Z'%20id='形状'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

News

Press Releases

WuXi AppTec Reports Strong Revenue Growth in 2021

2022/03/23

Revenue Up 38.5% Year-Over-Year to RMB22,902 Million

Net Profit Attributable to Owners of the Company Up 72.2% Year-Over-Year to RMB5,097 Million

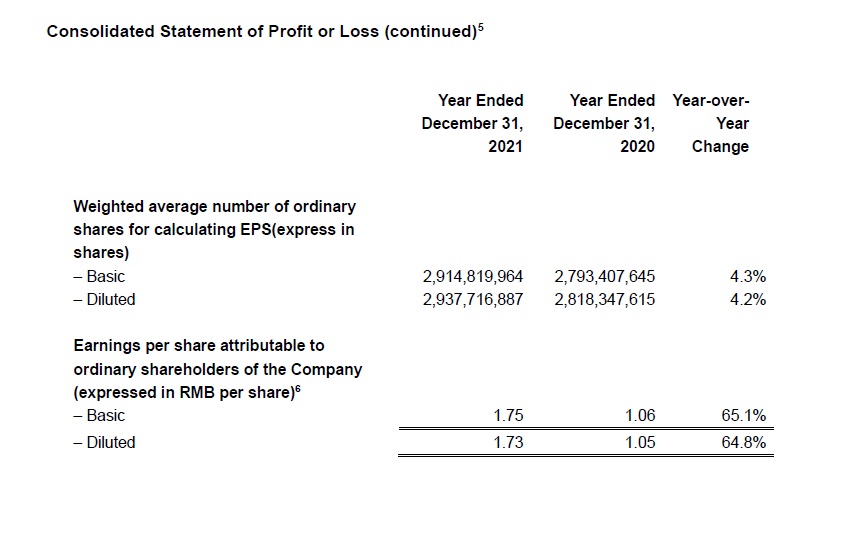

Diluted Earnings Per Share (EPS) Up 64.8% Year-Over-Year to RMB1.73

Adjusted Non-IFRS[1] Net Profit Attributable to Owners of the Company Up 41.1% Year-Over-Year to RMB5,131 Million

Adjusted Non-IFRS Diluted EPS Up 35.7% Year-Over-Year to RMB1.75[2]

(SHANGHAI, March 23, 2022) — WuXi AppTec (stock code: 603259.SH / 2359.HK), a global company that provides a broad portfolio of R&D and manufacturing services that enable companies in the pharmaceutical, biotech and medical device industries worldwide to advance discoveries and deliver groundbreaking treatments to patients, is pleased to announce its annual results for the year ending December 31, 2021 (“Reporting Period”).

This release provides a summary of the results and is not intended to be a comprehensive report. For additional information, please refer to the 2021 annual report and other relevant announcements published on the websites of the Shanghai Stock Exchange (www.sse.com.cn) and the Stock Exchange of Hong Kong (www.hkexnews.hk), and the designated media for dissemination of the relevant information. Investors are advised to exercise caution and be aware of the investment risks in dealing in the shares of the Company.

All financials disclosed in this press release are prepared based on International Financial Reporting Standards (IFRS), in currency of RMB.

The 2021 Annual Report of the Company has been audited.

2021 Financial Highlights

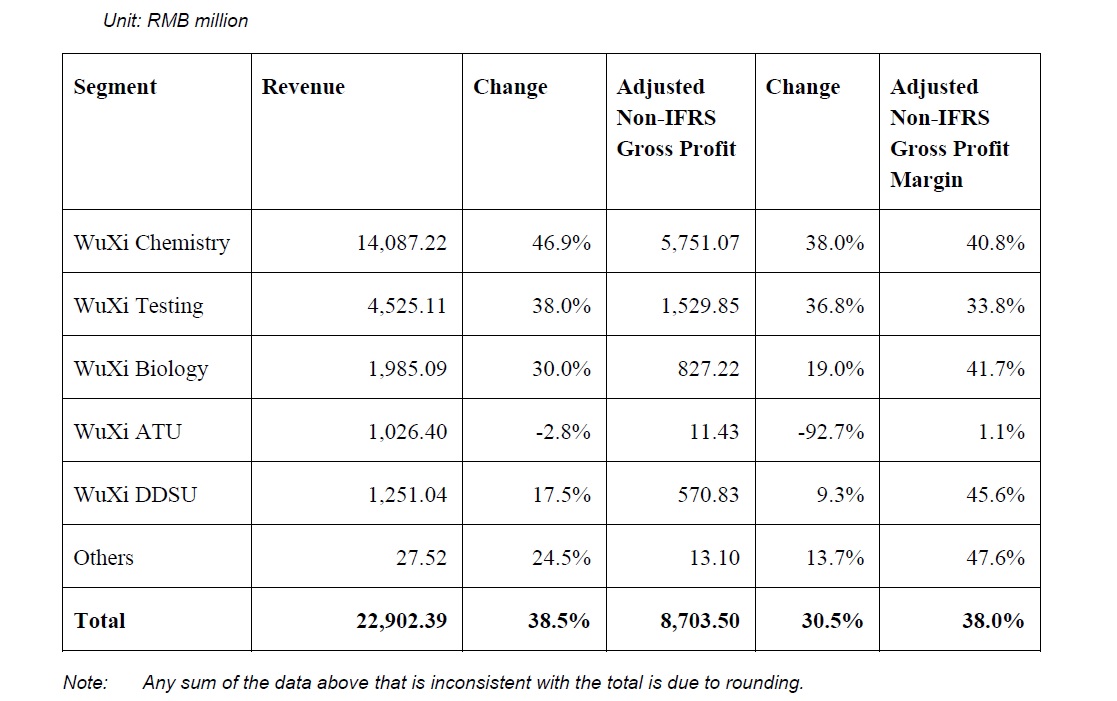

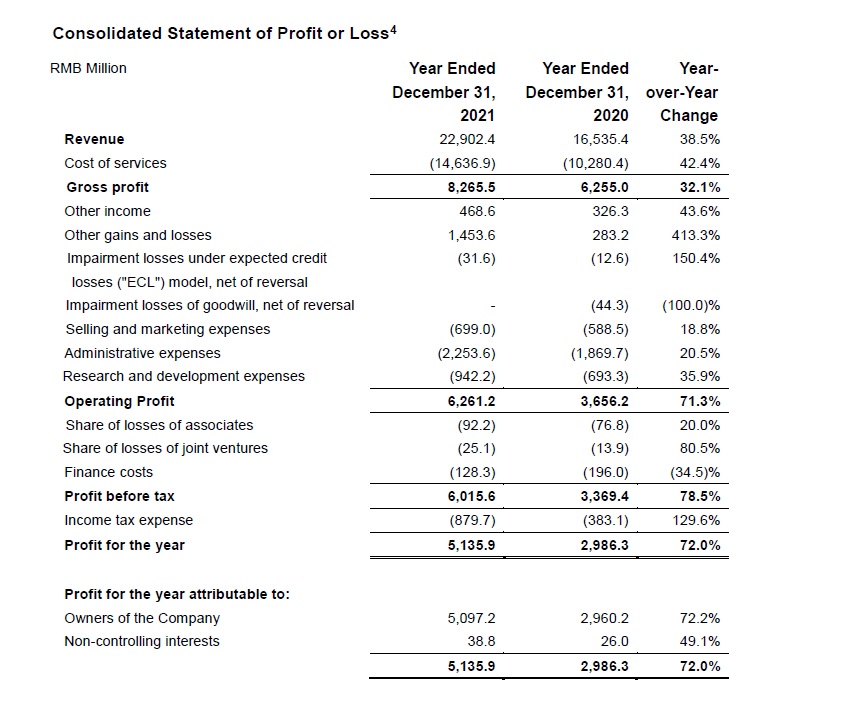

Revenue grew 38.5% year-over-year to RMB22,902 million. This is primarily attributable to the Company’s continued focus on leveraging its unique CRDMO business model to achieve synergy and strong growth across our business segments:

l WuXi Chemistry revenue grew 46.9% to RMB14,087 million and adjusted non-IFRS gross profit grew 38.0% to RMB5,751 million, with a gross profit margin of 40.8%.

l WuXi Testing revenue grew 38.0% to RMB4,525 million and adjusted non-IFRS gross profit grew 36.8% to RMB1,530 million, with a gross profit margin of 33.8%.

l WuXi Biology revenue grew 30.0% to RMB1,985 million and adjusted non-IFRS gross profit grew 19.0% to RMB827 million, with a gross profit margin of 41.7%.

l WuXi ATU revenue declined 2.8% to RMB1,026 million and adjusted non-IFRS gross profit declined 92.7% to RMB11 million, with a gross profit margin of 1.1%. WuXi ATU China subsidiary grew revenue by 87% year over year.

l WuXi DDSU revenue grew 17.5% to RMB1,251 million and adjusted non-IFRS gross profit grew 9.3% to RMB571 million, with a gross profit margin of 45.6%.

- IFRS gross profit increased 32.1% year-over-year to RMB8,266 million. Gross profit margin was 36.1%.[3]

- Adjusted Non-IFRS gross profit increased 30.5% year-over-year to RMB8,704 million. Adjusted Non-IFRS gross margin was 38.0%.

- EBITDA increased 62.2% year-over-year to RMB 7,624 million.

- Adjusted EBITDA increased 37.1% year-over-year to RMB7,592 million.

- Net profit attributable to owners of the Company increased 72.2% year-over-year to RMB5,097 million. The strong net profit growth is primarily attributable to robust revenue growth and continuous improvements to the Company’s operating efficiencies.

- Adjusted non-IFRS net profit attributable to owners of the Company increased 41.1% year-over-year to RMB5,131 million.

-Diluted EPS increased 64.8% year-over-year to RMB1.73, while adjusted diluted non-IFRS EPS increased by 35.7% year-over-year to RMB1.75.

2021 Business Highlights

- In 2021, demand for our services was strong and we grew our customer base to more than 5,700 active accounts by adding more than 1,660 new customers. We continued to optimize cross-platform synergies to better serve our customers worldwide, strengthen our unique competitive advantage as a fully integrated CRDMO (Contract Research Development and Manufacturing Organization) and CTDMO (Contract Testing Development and Manufacturing Organization), and provide one-stop services for our clients from discovery to development and manufacturing. Revenue growth was demonstrated across our expanding global customer base:

l Revenue from US-based customers grew 37% to RMB12,146 million; revenue from Europe-based customers grew 40% to RMB3,719 million; revenue from China-based customers grew 40% to RMB5,802 million; and revenue from other regions grew 41% to RMB1,234 million.

l We continued to expand our customer base and retain existing clients. During the Reporting Period, revenue from existing clients grew 29% to RMB21,295 million and new clients contributed RMB1,608 million in revenue.

l During the Reporting Period, revenue from the top 20 global pharmaceutical companies grew 24%, up to RMB6,733 million in revenue; revenue generated from all other customers grew 46% to RMB16,170 million.

l Our unique positioning across the pharmaceutical development value chain drove our “follow-the-customer” and “follow-the-molecule” strategies and enhanced synergies across our business segments. Customers using services from multiple business units contributed RMB19,639 million in revenue, growing 37% year-over-year.

- WuXi Chemistry: CRDMO integrated business model is the foundation for continued growth

l Revenue grew 46.9% to RMB14,087 million and adjusted non-IFRS gross profit grew 38.0% to RMB5,751 million, with a gross margin of 40.8%.

l Revenue from small molecule discovery services (“R”) grew 43.2% to RMB6,167 million.

i. Our industry-leading small molecule drug discovery platform delivered more than 310,000 custom synthesized compounds to our clients in 2021. Through our small molecule discovery services, we enabled our customers to accelerate their research while generating opportunities for our downstream business units. As part of our “follow the customer” and “follow the molecule” strategies, we established trusted partnerships with our global customers, which helped continue support for clinical and commercial projects and opportunities for the company. The small molecule discovery service laid a solid foundation to support the rapid and sustainable growth of our CRDMO business.

ii. We continued executing our “long-tail” strategy, and those customers demonstrated notable growth. During the Reporting Period, revenue from “long-tail” customers in our small molecule discovery service grew 71%, with its percentage of revenue contribution continuously rising as innovations are increasingly driven by small biotech companies.

l Revenue from our small molecule development and manufacturing (“D&M”) service grew 49.9% to RMB7,920 million.

i. During the Reporting Period, the Company added 732 new molecules to our project funnel for a total of 1,666 molecules, including 42 in commercial stage, 49 in phase III, 257 in phase II and 1,318 in phase I and pre-clinical stages.

ii. New modalities in business are also gaining strong momentum. During the reporting period, the number of oligonucleotide and peptide D&M clients increased 128% to 57, and the number of oligonucleotide and peptide D&M molecules increased 154% to 99. Revenue from oligonucleotide and peptide D&M grew 145%, reaching USD115 million.

iii. Our drug product (DP) business also made significant progress. The Shanghai Waigaoqiao (WGQ) site passed the first DP pre-approval inspection (PAI) by the US FDA in October 2021. During the same week, the WGQ site also passed two DP PAIs by China’s NMPA. Three successful DP PAIs in one week is a strong testament to WuXi AppTec’s robust quality system. By the end of 2021, we had four commercial DP projects and eight more DP projects in Phase 3 or NDA review stage.

l Capacity expansion of WuXi Chemistry continued accelerating in 2021:

i. In terms of capacity increase, we started operations at three facilities in Changzhou (Phase 2), Taixing and Wuxi city (oral & sterile filling DP plants). We also completed the construction of our facility in Changshu for scale-up and non-GMP manufacturing, and made significant progress in Changzhou Phase 3 capacity build-up, Taixing Phase 1 capacity build-up and selected a commercial manufacturing site in Delaware, US.

i. We completed the acquisition of a DP manufacturing facility in Couvet, Switzerland from Bristol Myers Squibb. The Company consolidated its contribution starting from July 2021.

l In addition to the progress made in 2021, we expect WuXi Chemistry to nearly double revenue growth in 2022 compared with that in 2021. This is a further validation of our CRDMO business model.

- WuXi Testing: strengthening synergies between preclinical and clinical testing services

l Revenue from WuXi Testing grew 38.0% to RMB4,525 million and adjusted non-IFRS gross profit grew 36.8% to RMB1,530 million, with a gross margin of 33.8%.

l Revenue from lab testing services grew 38.9% year-over-year to RMB3,045 million. Lab testing services revenue excluding medical devices testing grew 52% year over year.

i. The Company provides a full range of laboratory testing services to our customers, including DMPK (drug metabolism and pharmacokinetics), toxicology, and bioanalysis for drug development testing as well as medical device testing. We leveraged our integrated WuXi AppTec Investigational New Drug (IND) program (WIND) to generate preclinical data and prepare global regulatory submissions of IND packages, expediting the IND application process for many of our customers worldwide. Customers signed 149 WIND service packages with us in 2021, up 49% from 100 in 2020.

ii. Toxicology services achieved strong revenue growth of 63% year-over-year. We maintained our industry-leading position in Asia for drug safety evaluation services that meet global regulatory requirements.

iii. DMPK new modality related revenue grew significantly by 150% in 2021.

iv. The Company formed a cross-functional team between laboratory testing departments and the clinical CRO business unit to engage our customers once their projects are close to IND stage. We believe this business realignment will further strengthen the funnel flow from pre-clinical testing to clinical testing, creating synergy across our integrated testing platform.

l Revenue from clinical CRO & SMO (site management organization) grew 36.2% year-over-year to RMB1,480 million.

i. For clinical CRO, the Company provided services to around 240 projects, enabling our customers to obtain 19 IND approvals and file 12 BLA/NDA applications.

ii. For SMO, the Company continued its rapid expansion. Our SMO maintained more than 4,500 staff in 155 cities in China, providing services in over 1,000 hospitals. The team size increased 36% year-over-year, demonstrating strong market demand for our SMO services. In 2021, SMO enabled 25 new drug approvals versus 17 drug approvals in 2020.

l We anticipate that the revenue growth of WuXi Testing in 2022 will be consistent with its growth trajectory of the past few years.

- WuXi Biology: leading innovation in new modalities

l Revenue from WuXi Biology grew 30.0% to RMB1,985 million and adjusted non-IFRS gross profit grew 19.0% to RMB827 million, with a gross margin of 41.7%.

l The Company has the largest discovery biology enabling platform, with more than 2,200 experienced scientists who provide comprehensive biology services covering all stages and therapeutic areas of drug discovery. The Company has established 3 centers of excellence for NASH, anti-viral, neuroscience & aging. Discovery service focusing on cancer, rare & immune disease service also grew strongly. The Company launched the database of OncoWuXi 2.0, covering all immuno oncology tumor models, and also launched the product of WuXi IO Foundation, leveraging advanced technology platforms such as Multiplex-IF and digital imaging to precisely illustrate cancer cells, infiltrated immune cells and their spatial relationship within tumor microenvironment.

l The Company has a leading DNA Encoded Library (DEL) and hit compound generation platform. As of December 31, 2021, our DEL had more than 90 billion compounds, 6,000 proprietary scaffolds and 35,000 building blocks. More than 1,000 customers globally now use our DEL services. We have also launched the fourth-generation DEL kit in October 2021, which helped accelerate DEL’s revenue growth to 42% YoY in 2021.

l Through comprehensive integration of our DEL, protein production, and structure-based drug design (SBDD) capabilities, we have established a competitive Target-to-Hit platform to enable our customers’ drug discovery of small molecule drugs.

l The Company continues to build new biology capabilities related to new modalities, including oligo, cancer vaccine, PROTAC, viral vectors, novel drug delivery vehicles, etc. During the Reporting Period, revenue from new modalities and large molecules in WuXi Biology grew 75%, and its revenue contribution rose to 14.6% by the end of 2021, from 10.4% by end of 2020, suggesting that new modalities-related biology services have become an increasingly important growth driver. Among the new modalities-related biology services, oligonucleotide business grew quickly. The Company has established a world-leading comprehensive biology service platform for oligonucleotide and has a database with more than 50 drug targets, providing integrated services to several projects.

l We anticipate that the revenue growth of WuXi Biology in 2022 will be consistent with its growth trajectory of the past few years.

- WuXi ATU: CTDMO integrated business model hit a turning point and is expected to drive future growth

l Revenue from WuXi ATU declined 2.8% to RMB1,026 million in 2021; however, driven by strong demand for plasmids and lenti-viral vectors manufacturing, WuXi ATU’s China subsidiary generated strong revenue growth of 87% in 2021. This partially offset the decline at our Philadelphia site due to project BLA delays and the impact of COVID-19.

l During the Reporting Period, the Company focused on improving our CTDMO integrated enabling platform and strengthened testing services, capabilities, and capacities. We provided development and manufacturing services for 74 projects, including 58 pre-clinical and Phase I projects, 5 Phase II projects, and 11 Phase III projects.

l Capacity expansion of WuXi ATU continued in 2021:

i. Our integrated CTDMO site in Shanghai Lin-gang opened in October 2021. Its 15,300 square meters are equipped with 200+ independent suites and six complete production lines, which offer integrated development, manufacturing, and testing services for viral vectors and cell therapies to global clients.

ii. A newly built, 13,000 square meters testing facility in Philadelphia opened in November 2021, which tripled our testing capacity for cell and gene therapy products.

l Building on momentum in Q4 of 2021, 2022 will mark a turning point in WuXi ATU and we anticipate that WuXi ATU’s revenue growth in 2022 will exceed the growth rate of its industry sector.

- WuXi DDSU: enabling China-based customer innovation

l Revenue from WuXi DDSU grew 17.5% to RMB1,251 million and adjusted non-IFRS gross profit grew 9.3% to RMB571 million, with a gross margin of 45.6%.

l During the Reporting Period, our success-based drug discovery service unit filed INDs for 26 drug candidates and obtained 23 CTAs on behalf of China-based customers. As of December 31, 2021, we have cumulatively submitted 144 new chemical entity IND filings with the NMPA and obtained 110 CTAs, with one project in NDA review stage, three projects in Phase III clinical trials, 14 projects in Phase II clinical trials, and 74 projects in Phase I clinical trials. Upon products’ successful launch to the market by our customers, we will begin receiving royalty income.

l Among the 144 projects for which INDs were filed or are currently in clinical stage, about 70% of them rank in the top three in China in terms of drug development progress among same-class drug candidates.

l WuXi DDSU’s business will evolve in 2022 in order to meet China-based customers’ increasingly high expectations for projects to be delivered; as a result, we expect that WuXi DDSU’s revenue will be down somewhat in 2022 relative to that of 2021.

Continuous Improvements in ESG Management and Performance

As an innovative enabler, trusted partner, and contributor to the global healthcare industry, WuXi AppTec (“the Company” or “we”) insists on the sustainability development strategy and take the responsibility of the global citizen.

We continue to improve our ESG management by following international standardized system. Some of our main operational sites have obtained the certification of ISO 14001 Environmental Management System, ISO 45001 Occupational Health and Safety Management System, and ISO 27001 Information Security Management System. On the environmental side, we have developed an environmental action plan, and for the first time we are announcing specific targets to reduce our environmental impact. Compared to a 2020 baseline, by 2030 we are determined to reduce energy consumption intensity and carbon emission intensity by 25% respectively, and water use intensity by 30%. On the social side, we actively carried out ESG training for our employees and conducted key supplier ESG training and audit to create an excellent ESG atmosphere.

In 2021, our ESG performance was recognized by several international institutions. We received AA ESG rating from Morgan Stanley Capital International (MSCI), and were included in the Dow Jones Sustainability (DJSI) Emerging Markets Index for the first time. In addition, we received a B rating from the Carbon Disclosure Project (CDP) Climate Change Questionnaire.

We remain committed to “doing the right thing, and doing it right,” and will remain steadfast in our commitment to patients, customers, investors, employees, and communities to operate in a sustainable way both today and in the future.

Management Comment

Dr. Ge Li, Chairman and CEO of WuXi AppTec, said, “2021 was yet another successful year for WuXi AppTec. Our comprehensive enabling platform continued to support the growing needs of existing customers and attracted new ones throughout the healthcare industry. As part of our enduring commitment to serving our customers more effectively, we restructured our services into five new business segments in 2021. These five business segments reflect how we manage our business and also provide clearer transparency to our shareholders. We are confident that these five business segments will drive our growth for many years to come as we further enhance synergies, increase cross-selling, and deepen customer engagement across our diverse service offerings.”

Dr. Ge Li concluded, “The success of our unique CRDMO and CTDMO business models provides a foundation for reliable and continued long-term growth for our company and customers worldwide. The fundamentals of our business and its future outlook both remain very strong, and we will continue to invest in R&D service capabilities and capacities, particularly in new modalities and manufacturing. We expect to invest approximately RMB 9-10 billion in capital expenditures in 2022 to build new capacities for future growth. We are confident that these investments will better enable our customers worldwide to bring innovative medicines to patients in need – realizing our vision that ‘every drug can be made and every disease can be treated.’”

About WuXi AppTec

As a global company with operations across Asia, Europe, and North America, WuXi AppTec provides a broad portfolio of R&D and manufacturing services that enable the global pharmaceutical and healthcare industry to advance discoveries and deliver groundbreaking treatments to patients. Through its unique business models, WuXi AppTec’s integrated, end-to-end services include chemistry drug CRDMO (Contract Research, Development and Manufacturing Organization), biology discovery, preclinical testing and clinical research services, cell and gene therapies CTDMO (Contract Testing, Development and Manufacturing Organization), helping customers improve the productivity of advancing healthcare products through cost-effective and efficient solutions. WuXi AppTec received an AA ESG rating from MSCI in 2021 and its open-access platform is enabling more than 5,700 collaborators from over 30 countries to improve the health of those in need – and to realize the vision that "every drug can be made and every disease can be treated." Please visit: http://www.wuxiapptec.com

Forward-Looking Statements

This press release may contain certain “forward-looking statements” which are not historical facts, but instead are predictions about future events based on our beliefs as well as assumptions made by and information currently available to our management. Although we believe that our predictions are reasonable, future events are inherently uncertain and our forward-looking statements may turn out to be incorrect. Our forward-looking statements are subject to risks relating to, among other things, the ability of our service offerings to compete effectively, our ability to meet timelines for the expansion of our service offerings, our ability to protect our clients’ intellectual property, unforeseeable international tension, competition, the impact of emergencies and other force majeure. Our forward-looking statements in this press release speak only as of the date on which they are made, and we assume no obligation to update any forward-looking statements except as required by applicable law or listing rules. Accordingly, you are strongly cautioned that reliance on any forward-looking statements involves known and unknown risks and uncertainties. All forward-looking statements contained herein are qualified by reference to the cautionary statements set forth in this section. All information provided in this press release is as of the date of this press release and are based on assumptions that we believe to be reasonable as of this date, and we do not undertake any obligation to update any forward-looking statement, except as required under applicable law.

Use of Non-IFRS and Adjusted Non-IFRS Financial Measures

We provide non-IFRS gross profit, exclude the impact in revenue and cost from effective hedge accounting, share-based compensation expenses and amortization of intangible assets acquired in business combinations, and non-IFRS net profit attributable to owners of the Company, which exclude share-based compensation expenses, issuance expenses of convertible bonds, fair value gain or loss from derivative component of convertible bonds, foreign exchange-related gains or losses, amortization of intangible assets acquired in business combinations and goodwill impairment. We also provide adjusted non-IFRS net profit attributable to owners of the Company and earnings per share, which further exclude realized and unrealized gains or losses from our venture investments and joint ventures. Neither is required by, or presented in accordance with IFRS.

To better reflect the operation results and key performance, the Company has adjusted the scope of the foreign exchange related gains or losses by adjusting only the gains or losses that the management believes irrelevant to the core business. The comparative financial figures for the comparable periods have been adjusted to reflect the change of the scope.

We believe that the adjusted financial measures used in this press release are useful for understanding and assessing our core business performance and operating trends, and we believe that management and investors may benefit from referring to these adjusted financial measures in assessing our financial performance by eliminating the impact of certain unusual, non-recurring, non-cash and non-operating items that we do not consider indicative of the performance of our core business. Such adjusted non-IFRS net profit attributable to owners of the Company, the management of the Company believes, is widely accepted and adopted in the industry the Company is operating in. However, the presentation of these adjusted non-IFRS financial measures is not intended to be considered in isolation or as a substitute for the financial information prepared and presented in accordance with IFRS. You should not view adjusted results on a stand-alone basis or as a substitute for results under IFRS, or as being comparable to results reported or forecasted by other companies.

For more information, please contact:

Mr. Kyler Lei (for investors)

IR Director

Email: kyler_lei@wuxiapptec.com

Mr. Davy Wu (for media)

PR Director

Email: davy_wu@wuxiapptec.com

[1] To better reflect the operation results and key performance, we adjusted the scope of Non-IFRS, and the comparative financial figures for the comparable periods have been adjusted to reflect this change.

[2] Full year 2020 and 2021, we had a fully-diluted weighted average share count of 2,818,347,615 and 2,937,716,887 ordinary shares, respectively.

[3] If prepared under Accounting Standard for Business Enterprises of PRC, the gross profit grew 32.3% year-over-year to RMB8,310 million. Gross profit margin was 36.3%.

[4] If the sum of the data below is inconsistent with the total, it is caused by rounding

[5] If the sum of the data below is inconsistent with the total, it is caused by rounding

[6] In 2021, pursuant to the 2020 Profit Distribution Plan considered and approved by the shareholders’ general meeting, the Company issued 2 shares for every 10 shares of the Company by way of capitalization of reserve. In accordance with the regulations of the China Securities Regulatory Commission, the Company has adjusted the basic earnings per share and diluted earnings per share for the comparative period according to the 2020 Profit Distribution Plan.

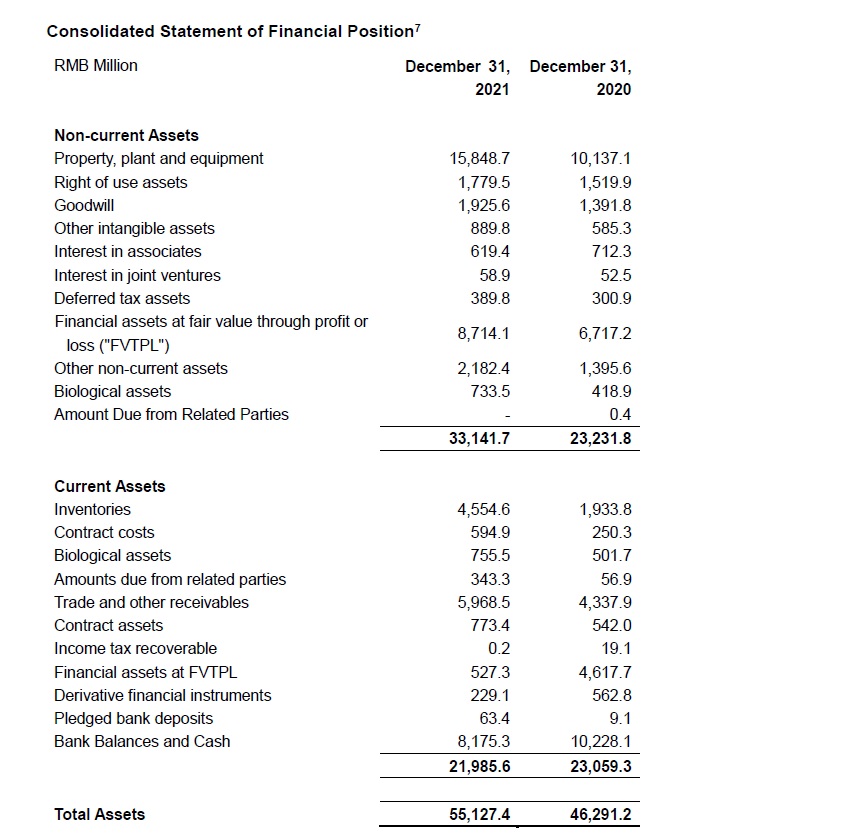

[7] If the sum of the data below is inconsistent with the total, it is caused by rounding.

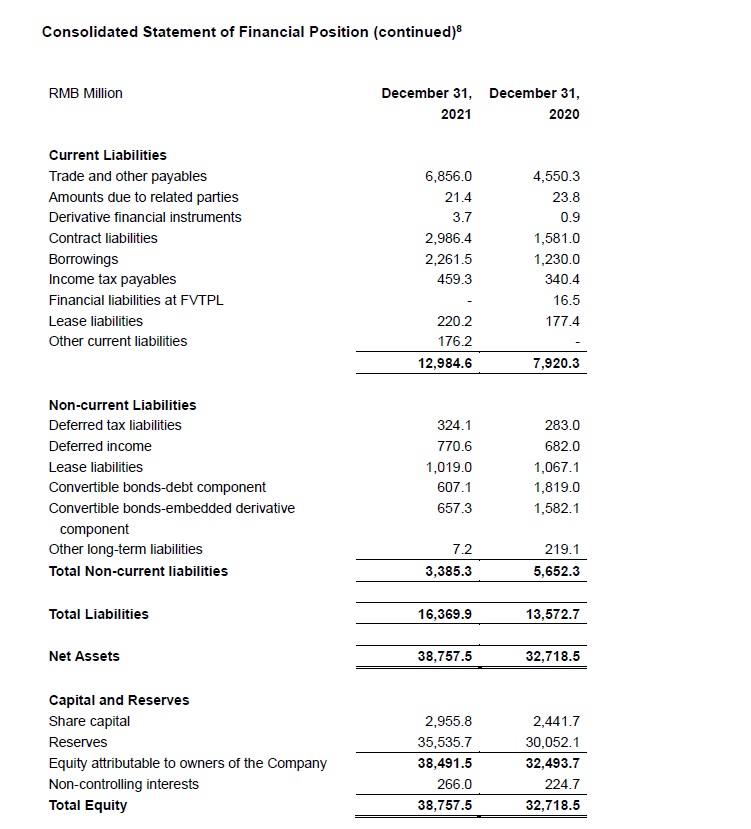

[8] If the sum of the data below is inconsistent with the total, it is caused by rounding.

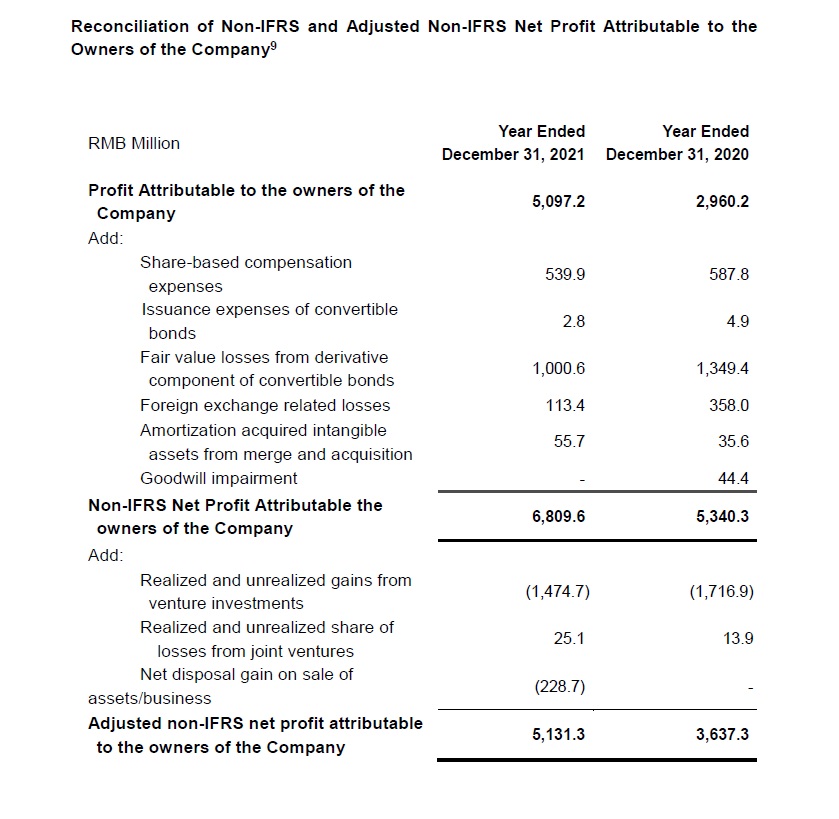

[9] If the sum of the data below is inconsistent with the total, it is caused by rounding.

The Company has adjusted the scope of the foreign exchange related gains or losses in the calculation of non-IFRS measures, by adjusting only the gains or losses that the management believes are irrelevant to the core business. The comparative financial figures for the comparable periods has been adjusted to reflect the change of scope.

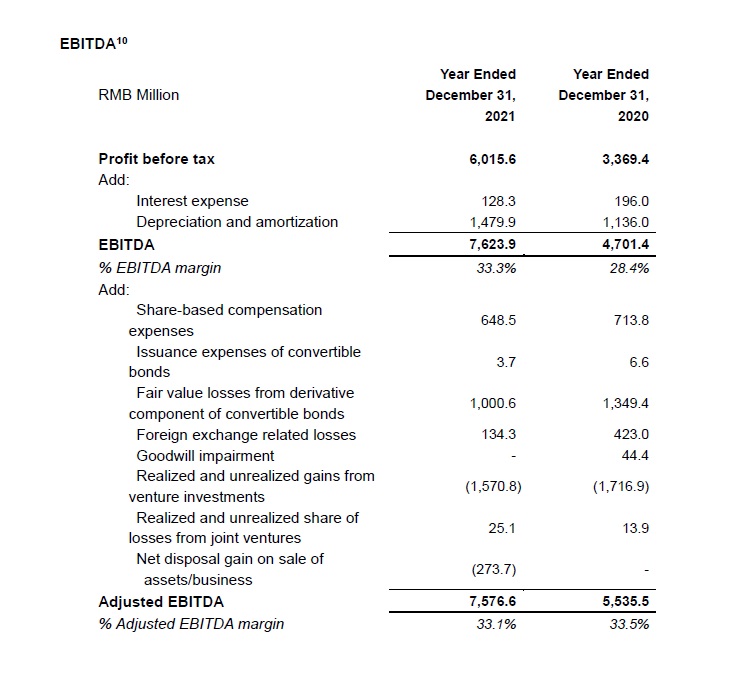

[10] If the sum of the data below is inconsistent with the total, it is caused by rounding.

The Company has adjusted the scope of the foreign exchange related gains or losses in the calculation of non-IFRS measures, by adjusting only the gains or losses that the management believes are irrelevant to the core business. The comparative financial figures for the comparable periods has been adjusted to reflect the change of scope.